Alıntı yaparak yanıtla

Alıntı yaparak yanıtlaBen daha kötü en alttan eşleşme bekliyorum ama gerçekleşmedi, bunda Viop30 a gelen son dakika alışları ve eşleştirme seansında diğer bankalara gelen alışlar etkili oldu!

|

|

|

|

Sağlam süzme bunlar, çok sağlam hemde...

Sabır Taşı...

Mantık sizi A noktasından B noktasına götürür. Hayal gücü ise her yere.

Platin Üye

Platin Üye

Ben daha kötü en alttan eşleşme bekliyorum ama gerçekleşmedi, bunda Viop30 a gelen son dakika alışları ve eşleştirme seansında diğer bankalara gelen alışlar etkili oldu!

Platin Üye

Niye performansi boyle oldu acaba? Hayal kirikligi yaratti. Tahsisli ile 1.30 olacak PD/DD mi acaba?Originally Posted by squidward

Geldim bir selam vereyim dedim.

Kıdemli Üye

Kıdemli Üye

Şimşek çakarsa belki yağmurda yağar serinleriz😋

Platin Üye

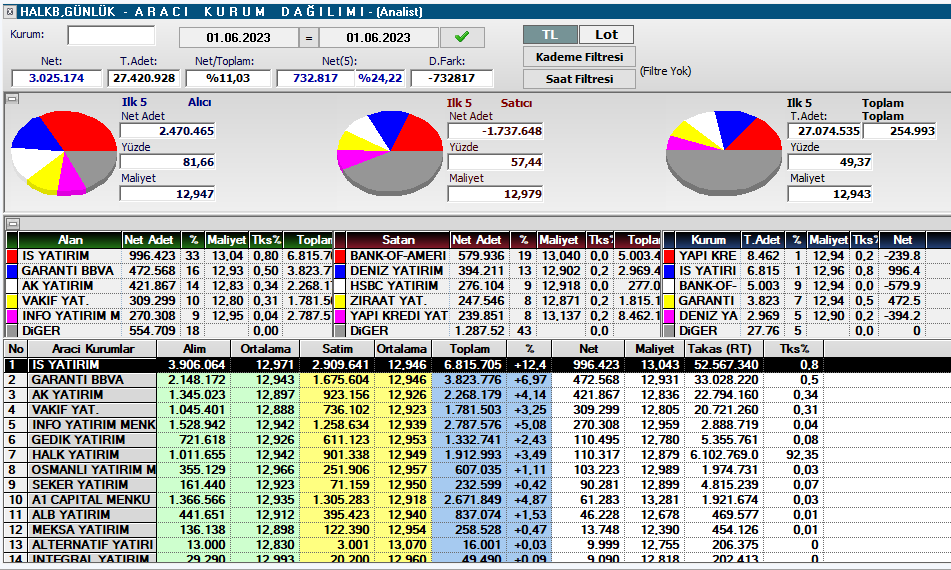

HALKB günlük, takas fena görünmüyor,

Platin Üye

Simsek gelince ne olacak ki? Ayni-tas-ayni-hamam ya da degisik-tas-ayni-hamam.

Platin Üye

Who Will Be Turkeys Next Finance Minister? Doesnt Matter

Analysis by Bobby Ghosh | Bloomberg

June 1, 2023 at 12:05 a.m. EDT

Who in their right mind would want to be Turkeys finance minister? The countrys economy is bleeding from years of abuse at the hands of President Recep Tayyip Erdogan, and most analysts agree that any chance of healing the wounds has been lost with his reelection.

The scuttlebutt from Ankara is that former finance minister and deputy prime minister Mehmet Simsek is being lined up for the job as economic czar. But if he ****s Erdogans new cabinet, expected to be announced tomorrow, it will mark a triumph of hope over experience.

Investors shouldnt make the same mistake. Nor should they put much stock in the presidents vague promise to appoint a team with international credibility to manage the nations finances. Until Erdogan explicitly abjures his absurd economic ideas the ones that have helped turn Turkey from the darling of emerging-market investors to a basket case on a par with Venezuela and Argentina any appointments he makes should be regarded as mere window dressing.

Simsek should know: Hes played that role before. In 2015, with investors growing nervous over Erdogans unorthodox economic ideas, the former Wall Street banker was appointed as deputy prime minister in an attempt to reassure markets. Simsek had been credited for maintaining fiscal discipline as finance minister between 2009 and 2015. His previous experience as a banker at UBS in Wall Street and Merrill Lynch in London was expected to count for a great deal with foreign investors.

But his role in the new cabinet was ill-defined, and within months his responsibilities had been trimmed. Many of the main levers of the economy were at the hands of those who followed Erdogans peculiar precepts on monetary and fiscal policy principally, his notion that lowering interest rates is the way to fight inflation. The markets had by then recognized that Simsek was a decoy, which ultimately made him superfluous. When the offices of prime minister and deputy prime minister were abolished in 2018, the president didnt care to find Simsek a new role in government. But after having sat demurely in the window, perhaps out of loyalty to his political master, Simsek had lost some of his credibility as an independent thinker.

That Erdogan is considering bringing him back is a sign he again sees Simsek as useful but for what, exactly? The president remains committed to lowering interest rates, which he regards as the mother and father of all evil. While he has acknowledged that inflation, currently more than 40%, is causing pain to Turks, his prescription for that hasnt changed. And many analysts fear he will take his reelection as an endorsement of his economic policies and an encouragement to keep flauting fiscal orthodoxy.

Nick Stadtmiller, head of product at Medley Global Advisors in New York, told Business News he expects interest rates will likely stay low, inflation will stay high, sovereign credit spreads will widen, while the currency will probably only slide slowly thanks to intervention.

So the return of Simsek to government will not, by itself, betoken real change. It will take much more to persuade the markets that he isnt again being used to dress Erdogans window.

Analysts will look closely at other appointments to the central bank, for instance to judge Erdogans willingness to cede authority in the management of the economy. But even a new slate of managers with international credibility will not suffice: So long as their jobs are the gift of the presidency, the officials will be constrained by his whimsy and caprice.

The closest thing to a guarantee of independence would be an amendment of the constitution that loosens the presidents grip on the levers of the economy. But having vastly expanded his powers through a referendum in 2017, Erdogan has shown no inclination to give any up.

In the absence of such evidence, investors should put little stock in the identity of next finance minister as they size up Turkeys prospects during Erdogans third decade at the helm.

Platin Üye

|

|

|

|

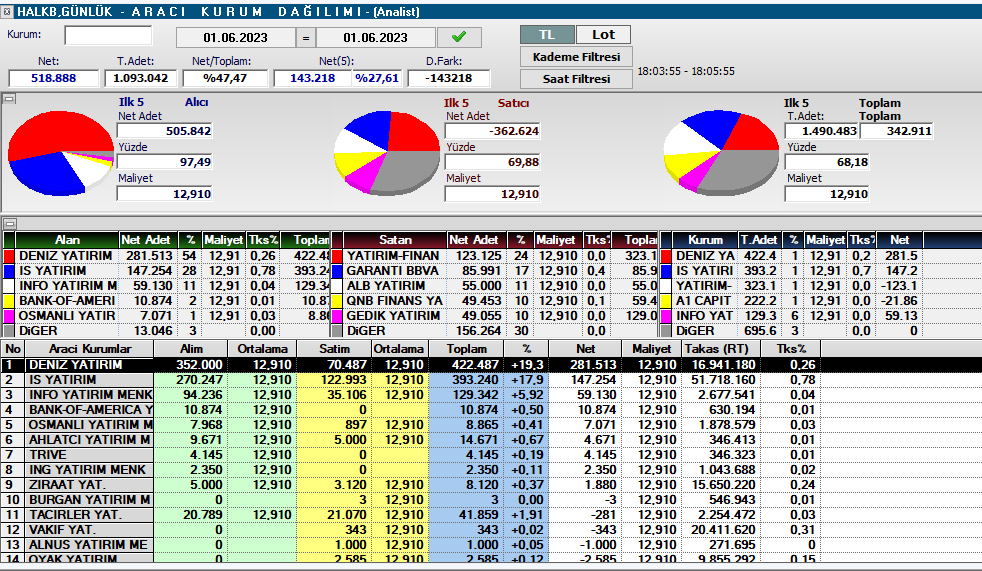

HALKB eşleşme takası, Deniz Yatırım 10 kademe üstten eşleştirdi, Viop30 a gelen alışla bütün bankalar yukarıdan eşleştiler,

Gönderi Kuralları

Gönderi Kuralları

Yer İmleri